Analysis Paralysis

"The only winning move is not to play"

Two themes have increasingly pressured financial markets over the last month: the AI revolution; and Iran de facto closing the Strait of Hormuz. Market participants were frustrated by the lack of volatility in December and January, but recent moves appear to have caused more misery than joy - with notable losses at some big hedge funds.

A reminder to be careful what you wish for.

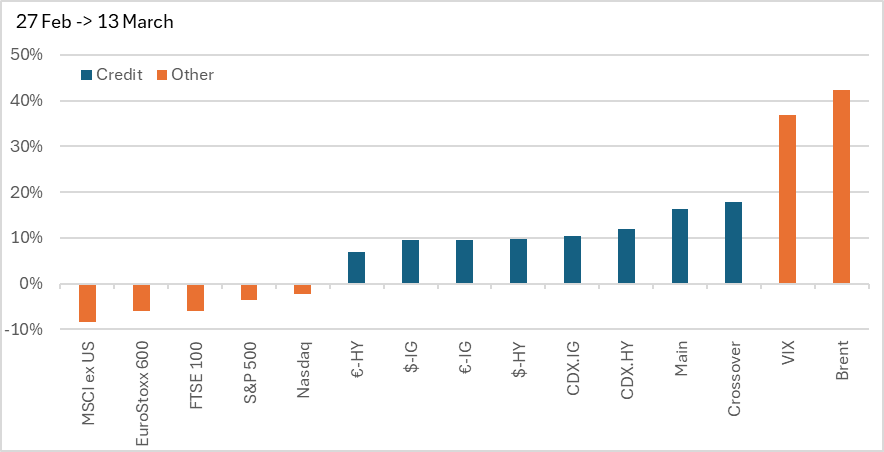

A particular pain point from my seat has been the way that parts of credit have run ahead of these events. European CDS indices1, in particular, have underperformed both equities and corporate bonds - moving with a high beta to volatility (VIX) and crude oil. This likely reflects the dominant size of multi-asset CTA flows in CDS index volumes, with non-credit investors using CDS as a relatively cheap hedge. But it sets up a tension in which, even if you anticipate more pain to come, it’s not obvious that credit is the best expression of this view.

And while cash spreads look expensive to CDS, the re-coupling trade is not a slam dunk either as the hardest hit market was European government bond (EGB) yields - which spiked higher as investors had flashbacks of 2022. As a result, corporate bond yields are now at their highest levels since 2024, which will be a strong support for the asset class if volatility eases.

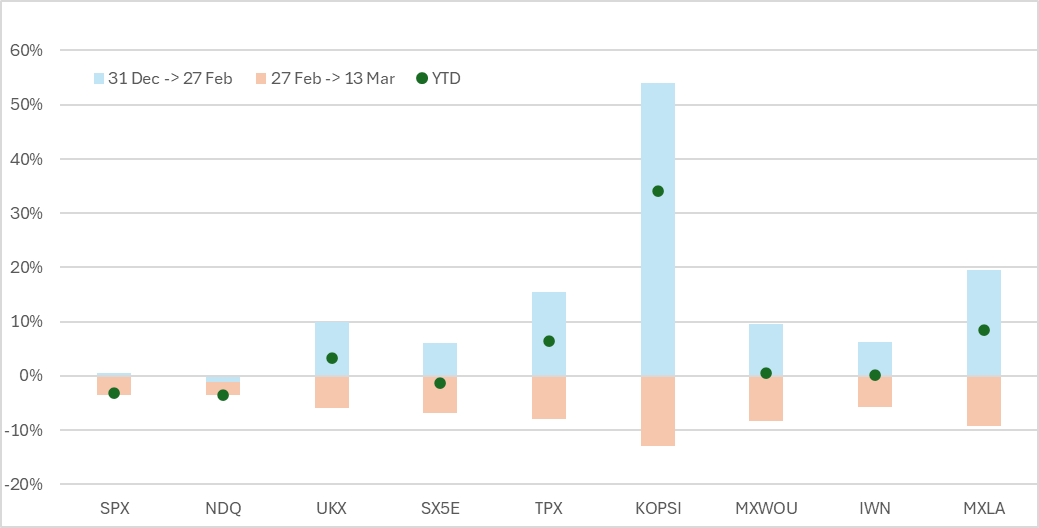

In contrast, despite aggressive moves from their peaks, global equities remain higher YTD ex. US, and only slightly lower in the US. Credit may be more asymmetric from an upside/downside perspective - approximately 6-to-1 weighing a recession against a retracement - but selling the asset class that has underperformed feels bad.

In this article, I look at the AI and Iran narratives. Both push up the risk of a US recession, but on different time-horizons. The Iran situation is both more acute and more likely to dissipate in the near term, but a Middle-East resolution would shift focus back to AI and software’s known unknowns.

Views expressed in this article are my personal opinions and do not reflect the opinions of any institution that I may be associated with. Nothing written in this article should be construed as investment or tax advice.

AI: All about intangibles

Since the end of January, the volume has been turned up on AI. Both OpenAI and Anthropic are preparing themselves to IPO, likely this year, triggering an increased cadence of model updates, stump speeches from the founders, and the release of agentic tools for enterprise use, as both companies build the case for why AI will dominate this century and why they will dominate AI.

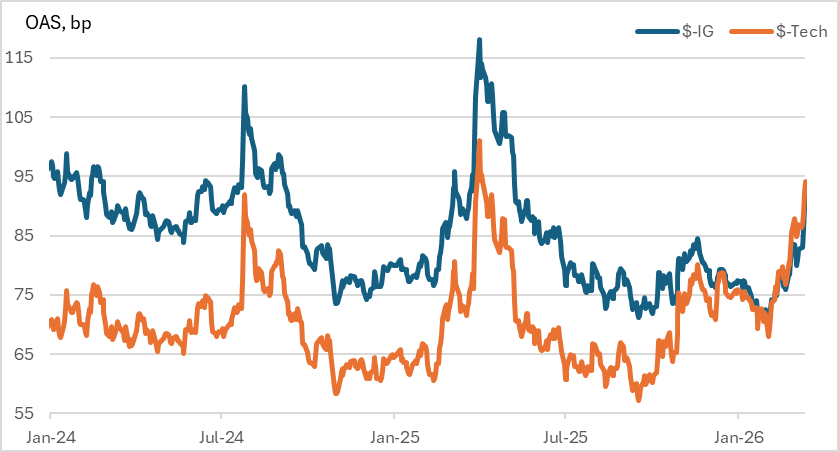

In parallel to this, Google and Amazon raised their CapEx forecasts for 2026 as they continued to message the rapidly growing demand for compute, driven by AI2. This led to huge bond issuance from both names, triggering a move wider in their own and adjacent credit spreads - albeit in the context of a weakening market.

The release and marketing of agentic coding agents has also raised existential questions about the future of software (and civilisation, if you believe Citrini). That has created a more credit-centric weakness in the market: issuance from Hyperscalers is an unfortunate technical headwind for spreads, but the potential for entire business models to go extinct is what really gets credit analysts excited.

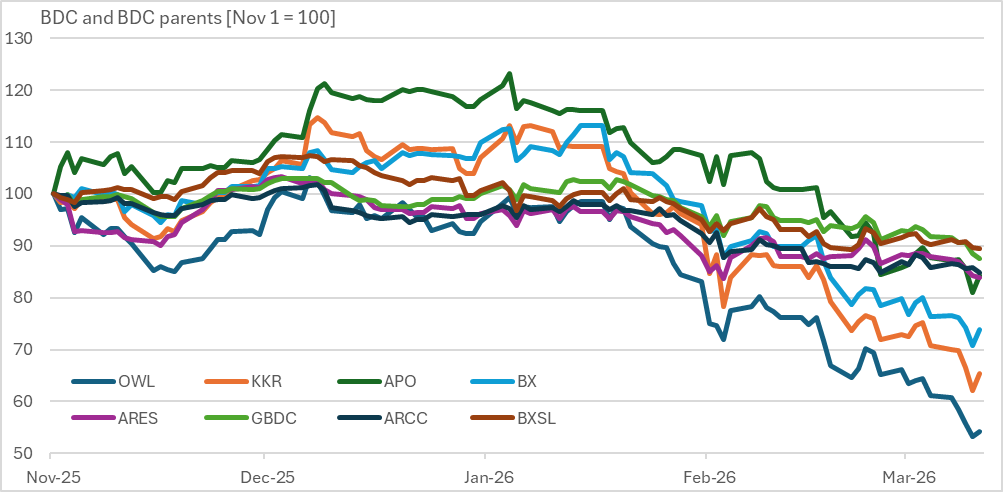

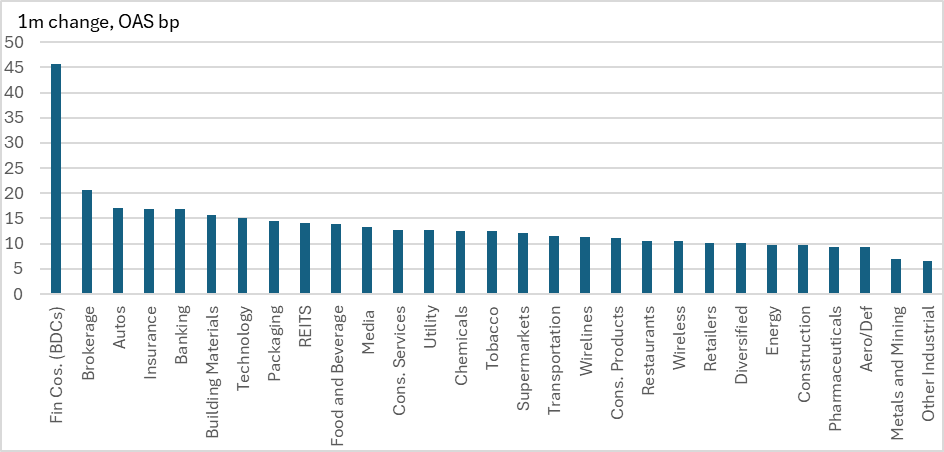

This is amplified further by the concentration of software/technology companies in both Private Equity (PE) and Private Credit (PC) portfolios. Private credit loans to software companies appear to be catnip for both the FT and Bloomberg, and the extensive (sometimes hysterical) reporting on this topic has found a focus in the form of BDCs3. A narrative and a trade that is working is a powerful combination.

With software historically under-represented in bond markets, certainly relative to its weight in equity indices, the BDC sector has become a kick-ball for investor fears over both private credit and AI. Long term, I think there is an opportunity in these bonds, but for now the sector remains toxic and thus untouchable.

The AI story clearly has legs. Proving the negative, that AI will not destroy a material number of these companies, will take many quarters or years. The BDC sector is small and many institutional investors do not have to hold it, making it likely that they walk away from the problem child, alleviating questions about their exposure to BDCs. That, in turn reinforces the downward spiral of these credits.

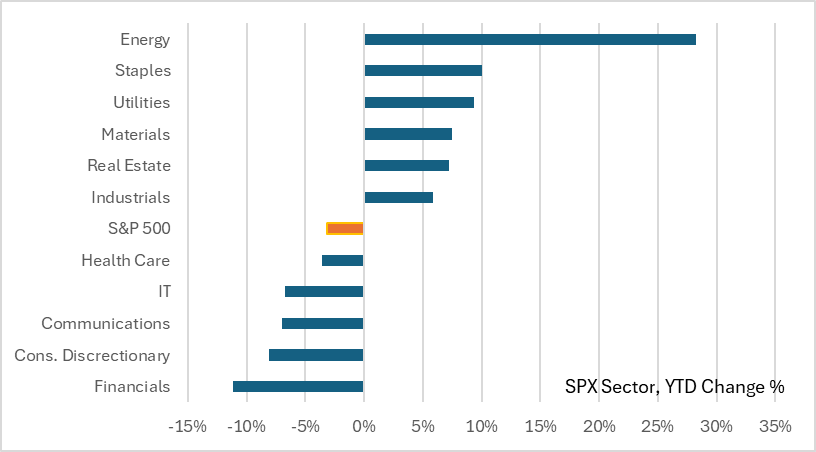

At the same time, given that Hyperscalers and AI are 34% of the S&P500, and Software is c. 8% it’s far from clear to me why credit would lead on this theme. Even if all the BDCs were to go away, credit should only feel a fraction of the downside that equity indices would suffer from those stocks going to zero… at least in theory. One factor that has helped drive this disconnect is that while software stocks are down, initially there were offsetting rises in Energy and Utility stocks that kept equity indices broadly unchanged - something that the credit market could not follow, as winning sectors were only able to “widen less”

Iran: The Taco that couldn’t (yet)

While the AI narrative pressured credit markets through February, the March breakdown has been driven by the US/Israel attack on Iran, and Iran’s subsequent closure of the Strait of Hormuz - a critical passage way for global trade. It is estimated that 20% of global oil production was shipped through the Straits last year, along with a large fraction of other critical commodities such as LNG, sulphur, urea, aluminium, and helium (critical in semi-conductor manufacturing).

Unsurprisingly oil spiked in response to these events.

More surprisingly, European government bonds were taken behind the shed by markets: a combination of reflexive memory of what happened in 2022 when Europe was cut off from Russian gas, and crowded positioning. While Europe’s demand for LNG from Qatar is acute, the European bond market is pricing in an extended inflationary spike - in contrast, oil and gas curves remain deeply backwardated, pricing a decline in oil prices over the next 12 months from $103 to $77.

More broadly, the market reaction to the Iran war has been relatively sanguine thus far - it took almost a week before markets really started to move. That may be because investors anticipated that Trump would quickly TACO when faced with significant rises in oil prices, given the sensitivity of the US public to pump prices. Indeed, the last few days have seen, between repeated bluster and showmanship, several attempts to declare mission accomplished which the market is interpreting as a precursor to de-escalation and a re-opening of the Strait. If Trump is about to TACO, then markets that have not moved are correct, and those that have moved will sharply reverse.

However, this assumes that re-opening the Strait is a unilateral decision that the PoTUS can make at any time. But it isn’t. Re-opening the Strait requires the Iranians (and to a degree, Israel) to play ball. And while Iran’s conventional military appears to have been massively degraded, it is almost impossible (and incredibly expensive) to completely eliminate asymmetric attacks on shipping. Meanwhile, there is no signal that Iran’s enriched uranium has either been secured or destroyed.

President Trump’s recent comments smell like weakness to me - a signal that he wants the fastest possible resolution, and is willing to accept a very diffuse and vague definition of win if it allows him to walk away from the situation with the Strait reopened. That is succour for markets.

What’s less clear to me is whether Iran will use the current weakness to broker a deal, or hold out knowing that every passing day puts more pressure on the US - at the cost of a further degradation of their own assets. Trump’s philosophy of escalate to de-escalate dictates that he will attack when unable to unilaterally resolve the situation. The bombing of Karg Island fits this pattern perfectly and escalation will, by definition, keep the Straits closed and markets under pressure for now.

We have got used to reading when President Trump is likely to fold, but the new Ayatollah is a known unknown. This makes me confident that I do not have any advantage in calling Iran’s next steps - and that watching from the sideline is the best course of action for now.

Conclusion: Sidelined by the wrong sort of volatility

Currently, both the Iran and AI themes are aligned in pushing up fears of a US/global recession. If the Strait is closed for several months, with energy prices held higher for an even longer period due to production declines and well shut-ins, then Europe will suffer a nasty stagflationary shock. Even if disruption only lasts another week, risk assets are far from pricing a recession and so prices can continue to decline (and spreads widen) until a resolution is forthcoming.

But like every US policy under Trump, a resolution could be found at any moment. The complication with Iran is that it cannot be a unilateral capitulation - it requires Iran to play-ball and, while they are under intense pressure, the decentralised nature of their military doctrine makes them less predictable. The market has already traded ten of the last zero resolutions, and the risk is that investors capitulate before Iran. The recession risk is acute, but so is the reversal risk.

In contrast, AI cannot be put back in Pandora’s Box and we know it. My view remains that we are less than half-way through the AI cycle, but BDCs are a weakness in credit that is not going to be cured - the question is can it be cauterised before it infects the rest of the public market? These concerns will remain an overhang for quarters, likely remaining unresolved until H2 at the earliest.

It was relatively easy to short credit in the first few days of the conflict4, because almost nothing was priced into credit and so the risk of escalation offered a truly asymmetric opportunity. But that is no longer the case; credit is ahead of other risk assets in pricing in a longer closure of Hormuz. With no advantage on calling Iran, it behoves us to do less: for real money that means hugging benchmarks; for leveraged investors double-checking that market beta really is hedged.

While credit will retain its beta to oil moves, this is now a double-edged sword and we have not yet seen a disorderly widening that creates true alpha opportunities, but hey… we just might get it.

Views expressed are the author's own and do not reflect those of any associated institution. The author's employer and its personnel may hold positions aligned with or contrary to the views expressed here. Views reflect the author's thinking at the time of writing and the author makes no commitment to publish updates.

Financial derivatives that buy or sell default protection on a basket of corporate credits.

It bears noting that much of the demand for AI at Google is coming internally, which says something to me about the somewhat closed-loop that is the AI ecosystem.

Business Development Corporations are, to all intents and purposes, a tax-wrapper for investors. The BDC is able to pay tax-free dividends provided that it holds a relatively narrowly-defined universe of debt-instruments, and distributes substantially all of the income generated by those loans.

This is easy to say in hindsight. At the time I was busy criticising Citrini, but thanks to those who reached out to me in the first few days to discuss the topic in real time.